Economy and Society: February 25, 2026

In this week’s edition of Economy and Society:

- JPMorgan confirms closing Trump accounts after Jan. 6

- House committee questions CalPERS over ESG investing

- Oklahoma tobacco fund adopts anti-ESG investment policies

- ESG legislation update

- Apple removes ESG metrics from executive compensation

- Goldman ends DEI requirements in board nominations

In Washington, D.C.

JPMorgan confirms closing Trump accounts after Jan. 6

What’s the story?

JPMorgan Chase acknowledged in a court filing that it closed the bank accounts of President Trump (R) and several of his businesses in February 2021, following the Jan. 6, 2021, breach of the U.S. Capitol. The bank's former chief administrative officer, Dan Wilkening, wrote in the filing that JPMorgan informed Trump that certain accounts maintained with the bank's private bank and commercial bank divisions would be closed. JPMorgan has never previously admitted in writing that it closed Trump's accounts, citing bank privacy laws.

The acknowledgment came in response to Trump’s $5 billion lawsuit, which alleges JPMorgan terminated the relationship for political reasons and disrupted his business operations. The bank filed the document as part of its effort to move the case from Florida state court to federal court and to shift jurisdiction to New York, where the accounts were located.

Why does it matter?

The case centers on claims of political discrimination and debanking, a term used when a bank closes customer accounts or declines to provide financial services. Trump’s attorneys said the filing confirms their claim that JPMorgan unlawfully closed his accounts. JPMorgan said the lawsuit lacks merit.

Since President Trump returned to office, federal banking regulators have moved to limit the use of reputational risk as a basis for denying financial services. In his Aug. 7, 2025 executive order, Guaranteeing Fair Banking for All Americans, Trump directed federal banking regulators to remove references to reputational risk from supervisory guidance and examination materials where it could result in politicized or unlawful debanking. The order also instructed regulators to consider rescinding or amending regulations that could allow such practices. The lawsuit may shape how courts evaluate banks’ discretion to terminate customer relationships under this new regulatory framework.

What’s the background?

Debanking became a national issue during the Obama administration after U.S. Rep. Darrell Issa (R-Calif.), then-chairman of the House Committee on Oversight and Government Reform, issued a staff report in 2014 alleging that the Department of Justice's Operation Choke Point pressured banks to stop serving gun stores, payday lenders, and other lawful businesses.

Trump originally filed suit in the Florida 11th Circuit Court in Miami-Dade County, where his primary residence is located. He alleged trade libel and violations of state and federal unfair trade practices laws. JPMorgan has sought to move the case to federal court in New York.

Trump has also filed a separate lawsuit against Capital One in March 2025 alleging similar conduct.

House committee questions CalPERS over ESG investing

What’s the story?

Members of the House Committee on Education and Workforce — including Chairman Tim Walberg (R-Mich.), Subcommittee Chairman Rick Allen (R-Ga.), and Subcommittee Chairman Kevin Kiley (R-Calif.) — sent a Feb. 12, 2026 letter to Theresa Taylor, president and vice chair of investment at the California Public Employees’ Retirement System (CalPERS), requesting documents related to the pension fund’s environmental, social, and governance (ESG) investing.

Walberg, Allen, and Kiley focused specifically on CalPERS' investments in the Clean Energy and Technology Fund (CETF), a private equity fund. The letter alleges that CalPERS invested more than $468 million in CETF starting in 2007 and that the investment's value had fallen to less than $138.1 million as of March 31, 2025 — a decline of 71%.

The lawmakers wrote that they seek to determine "whether CalPERS is undermining this requirement by prioritizing a radical Environmental, Social, and Governance (ESG) agenda over its obligation to its beneficiaries, which will inform its potential reforms to ERISA and the Code." They gave CalPERS until Feb. 27, 2026, to provide the requested information. The committee has no enforcement powers and cannot bring litigation against CalPERS, though it could refer findings to the Department of Justice.

Why does it matter?

Walberg, Allen, and Kiley question whether CalPERS violated the Internal Revenue Code's exclusive benefit requirement, which says that public pension plans receiving tax subsidies must operate "for the exclusive benefit of [an employer's] employees or their beneficiaries" under 26 U.S.C. § 401(a).

The lawmakers also raised concerns about whether CalPERS complied with California's constitutional requirement that pension assets be held "for the exclusive purposes of providing benefits to participants in the pension or retirement system and their beneficiaries and defraying reasonable expenses of the plan."

CalPERS is the largest public pension system in the United States. The lawmakers said their inquiry would inform potential changes to federal law, including the Employee Retirement Income Security Act of 1974 (ERISA) and the Internal Revenue Code. Currently, ERISA does not apply to governmental plans such as CalPERS, though the letter suggests Congress may consider extending such requirements.

What’s the background?

CalPERS published its first report on sustainable investing in 2012, titled "Towards Sustainable Investment: TAKING RESPONSIBILITY," which traced the pension fund's corporate governance and sustainability work back to 1984. The pension fund currently operates a Sustainable Investments Program and a $100 Billion Climate Action Plan.

Walberg’s inquiry builds on a July 29, 2024 letter that then-Chair Virginia Foxx (R-N.C.) sent to CalPERS regarding its participation in a Biden-Harris administration initiative involving public and pension capital.

In the states

Oklahoma tobacco fund adopts anti-ESG investment policies

What’s the story?

The Board of Investors for the Oklahoma Tobacco Settlement and Endowment Trust (TSET) voted 3-1 on Feb. 18, 2026, to revise its investment policy statement to incorporate what it calls Oklahoma Values and anti-ESG criteria into investment decisions, asset manager selection, and proxy voting. The board oversees a $2.2 billion tobacco settlement fund, a constitutionally created state trust funded from the 1998 Master Settlement Agreement with tobacco companies.

The changes follow recommendations from Oklahoma Treasurer Todd Russ (R). Under the new policy, TSET will adopt proxy voting guidelines that Bowyer Research, an independent proxy advisory firm, created. Jerry Bowyer presented the guidelines to the board by video and said Oklahoma is the first state to adopt them. The policy also incorporates an Oklahoma Values Alignment Assessment that Innovest, TSET's investment consultant, developed in 2025.

Board member John Waldo, an appointee of State Auditor and Inspector Cindy Byrd (R), voted against the changes.

Why does it matter?

The vote represents Oklahoma's most direct adoption of anti-ESG investment criteria for a state trust fund. Russ said the changes would give the state more control over how asset managers vote shares in publicly traded companies and would reinforce the importance of the oil and gas and agriculture industries to the state's economy. Bowyer told the board that a review of TSET's past proxy votes showed some asset managers voting "against the economic values of the state."

The policy changes align with recent actions by other Republican state officials opposing ESG investing. Russ chairs the Oklahoma State Pension Commission, which voted last week to review how asset managers vote proxies on their behalf. The vote followed a December executive order by President Trump (R). The commission's attorney reminded Russ that federal executive orders do not bind state pension systems, which have their own boards with fiduciary duties to members.

What’s the background?

Republican lawmakers and officials in multiple states have moved to restrict ESG considerations in public investments. Oklahoma lawmakers passed House Bill 2034 in 2022, a law modeled on Texas legislation that directed Russ to create a list of financial institutions the state deemed to be boycotting the oil and gas industry. Russ issued three versions of that list, which targeted Bank of America, State Street Corp., BlackRock Inc., and Barclays PLC.

An Oklahoma County district judge placed the law under permanent injunction in September 2024 after a state retiree filed a lawsuit challenging it. The Oklahoma Supreme Court is now reviewing the law.

A U.S. District Court judge in Texas overruled a similar Texas law on Feb. 4, 2026, holding that it violated First Amendment free-speech protections. Texas said it would appeal.

Two bills addressing how state pension systems cast proxy votes — HB 4428 and HB 4429, sponsored by House Speaker Kyle Hilbert (R-Bristow) — have passed initial committee votes in Oklahoma. Russ said he did not request the bills and had not discussed them with Hilbert.

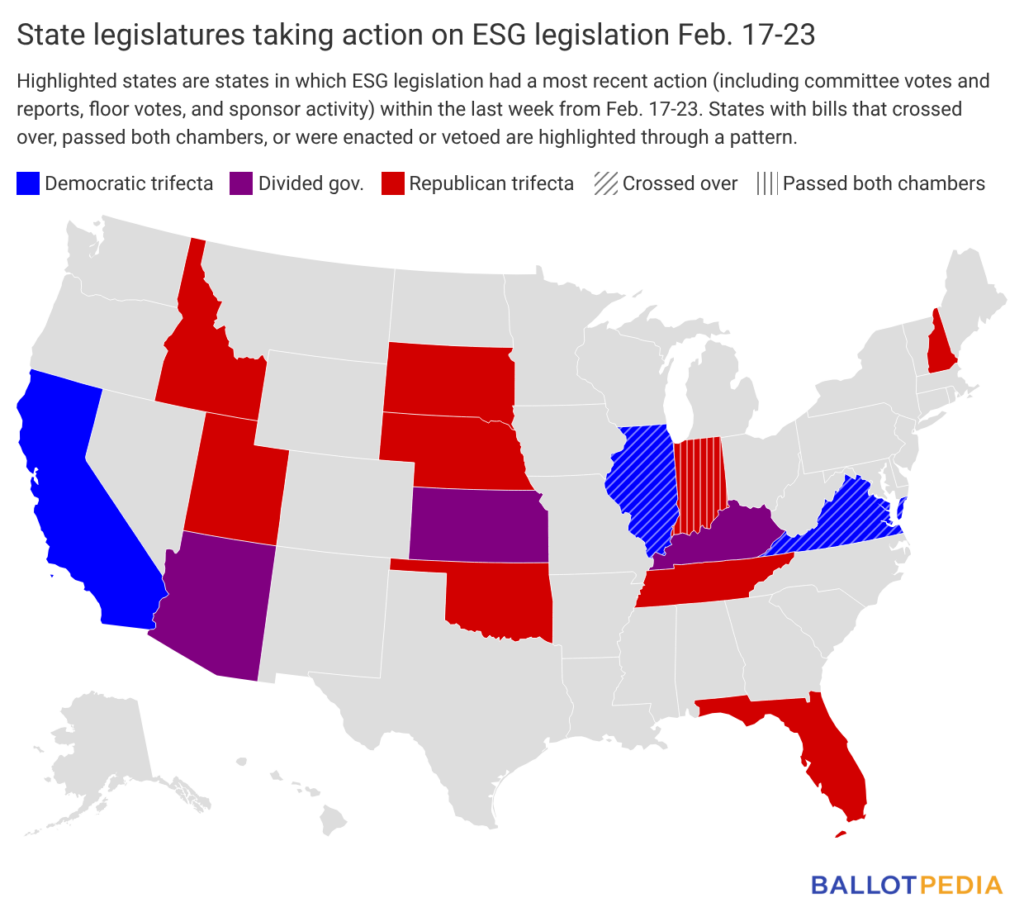

ESG legislation update

Fifteen states took action on 20 ESG-related bills last week (since Feb. 17).

Indiana HB 1273, as introduced, would require proxy advisory firms to disclose whether ESG-related recommendations against company management are supported by written financial analysis. The bill would also require proxy advisors to provide that information to interest holders, company management, and the public.

States with legislative activity on ESG last week are highlighted in the map below. Click here to see the details of each bill in the legislation tracker.

On Wall Street and in the private sector

Apple removes ESG metrics from executive compensation

What’s the story?

Apple removed ESG metrics from its executive compensation plan for 2025, according to a corporate filing the company made in January 2026. The company had used an ESG modifier since 2021 that allowed its board to adjust annual bonuses for CEO Tim Cook and other top executives by as much as 10% based on performance measures including greenhouse gas reductions and renewable energy use among suppliers.

Why does it matter?

Apple joins several major U.S. corporations that have recently eliminated ESG factors from executive pay calculations. Starbucks, Salesforce, Mastercard, and Procter & Gamble made similar decisions. Many large companies began removing diversity targets from executive compensation packages two years ago. Environmental measures tied to climate emissions now face comparable treatment.

What’s the background?

In December 2025, Apple announced that Lisa Jackson, its vice president of environment, policy and social initiatives, would retire in late January 2026 without a direct replacement. Jackson had led Apple's sustainability efforts for more than a decade, including the company's transition to renewable energy sources and its $100 million racial equity and justice program.

Goldman ends DEI requirements in board nominations

What’s the story?

Goldman Sachs will no longer consider race, gender, and sexual orientation when evaluating potential board members, according to The New York Times. The change followed a proposal from the National Legal and Policy Center, a nonprofit group that promotes ethics in public life. Goldman agreed to drop diversity criteria and the National Legal and Policy Center withdrew its proposal.

Why does it matter?

The decision marks another retreat from diversity, equity, and inclusion (DEI) mandates that Goldman Chief Executive David Solomon had previously championed. In 2020, Solomon said Goldman would not take a company public in the United States or Europe unless it had at least one diverse board member, a threshold the bank raised to two diverse members by 2021. Goldman dropped that underwriting policy in February 2025, the same month it eliminated explicit racial and gender goals for recruiting classes.

Other corporations have made similar decisions during the Trump administration. The Equal Employment Opportunity Commission opened investigations into diversity hiring practices at law firms and Nike in February 2026.

What’s the background?

The National Legal and Policy Center has pressured multiple companies to eliminate DEI policies, securing similar agreements with American Express and Deere & Company. At Goldman's 2025 annual shareholder meeting, the group praised the bank for rolling back DEI programs but proposed eliminating diversity goals tied to executive compensation. The board recommended against that proposal, and fewer than 5% of shareholders voted to support it.

Goldman's reversal contrasts with the bank's public position in January 2025, when Solomon and J.P. Morgan CEO Jamie Dimon both opposed shareholder proposals from conservative groups seeking to end DEI initiatives.

{kind=link}